Having an emergency fund is foundational to healthy finances and our pursuit of financial independence. From an unexpected car repair to the loss of a job, the primary job of an emergency fund is to help you weather unexpected financial challenges that could derail your financial progress. Depending on your situation, you may have anywhere from $1,000 upward to 6 months worth of expenses in a readily accessible account standing watch over your financial castle while you sleep a little more soundly. As important as that is, I want to talk here about the important side-hustle I have assigned my monetary firemen as they wait in the station training and polishing the emergency fund fire truck: self-insurance.

By strategically managing my insurance deductibles and not purchasing the myriad of minor insurance products on the market, I have been able to save a lot of money, and hopefully you can too.

In a nutshell, self-insurance is a financial strategy where you set aside money to pay for losses instead of buying insurance. It’s also known as self-funding. You save money instead of paying premiums to an insurance company. You pay for losses out of your own pocket instead of filing a claim.

To be clear, traditional insurance is an important financial tool to mitigate risks from rare, but costly, catastrophic events such as a house fire, a lawsuit from a car crash, death, or other major liabilities. Insurance can also be helpful when more common events might be devastating to your finances. When I was younger (and poorer), a new car tire was a major expense in my budget, whereas today I can afford to replace a car that is totaled. So as my emergency fund strengthened, my ability to self-insure also increased.

Insurance companies are businesses and make money from the premiums we pay – a lot of money when nothing happens, and a little less when they need to pay significant claims. They take advantage of our salience bias – a cognitive bias that predisposes us to focus on what is the most prominent, visible, or emotionally striking events in our environment. Insurance companies monetize our fears. They also play on our desire to conform (e.g., “9,384 people have insured this trip”). Almost everyone has a memorable story of when they did use their warranty or travel insurance or when it might have been useful (like the one time I spilled water on my 8-month old $1,000 laptop), but while memorable, these stories represent a small minority of our total experience with insurable products.

Like investing in the stock market, self-insurance requires risk tolerance and time. While an insurance company spreads risk across many participants, self-insurers spread risk across all types of insurance products and over time. Instead of looking at each situation individually (e.g., should I pay $30 to cover this $1000 airfare?), we look at all of our family’s self-insurance opportunities over time. For example, paying to replace a phone dropped in the water once in 15 years is more than offset by not paying for phone replacement insurance (at $100+ per phone per year) for a family’s four’s phones for that same period. The total of all the premiums for unused insurance for every flight, hotel, electronics items, etc., would far exceed the combined total of the replacement costs I actually incurred from self-insurance.

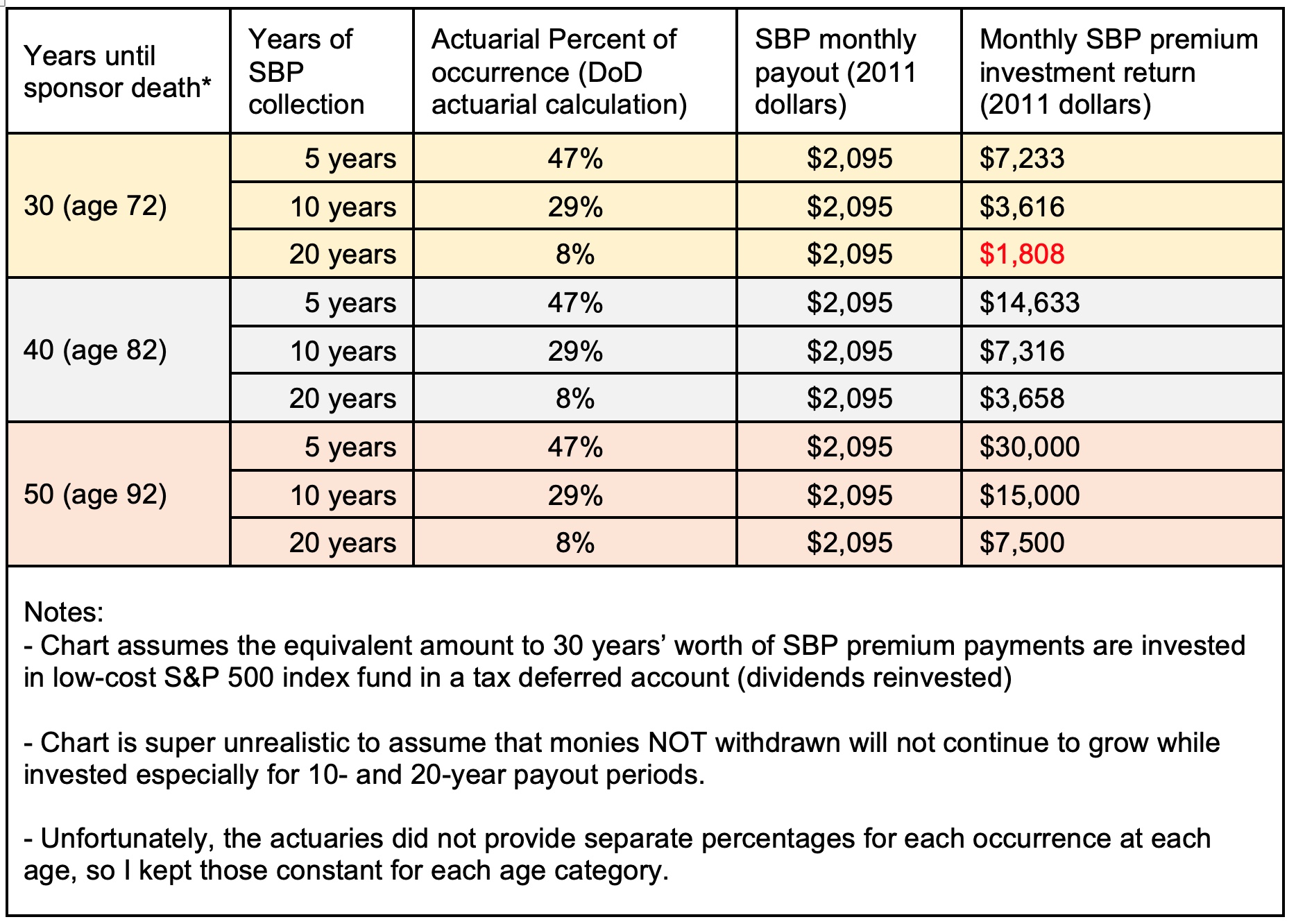

I buy insurance for catastrophic liability to include home (high deductible), car (high deductible), umbrella, and term life (never “whole” or “permanent” life!). But my wife and I skipped survivor insurance for my pension and there are other areas, listed below, in which my self-insurance strategies have saved me tens of thousands of dollars (not including compounded returns from investing the money instead) over the past three decades.

Auto collision and comprehensive

I drive well. My wife drives well. In our 79 years of combined driving history we have had only 3 at-fault claims (one involving another vehicle). The last one was 11 years ago. My two kids are both safe drivers. They have had zero at-fault claims in their 12 combined years of driving–the highest risk time for young drivers. Our vanity is not insulted if we have superficial scratches on the vehicle (whether caused by us or someone else) – if the car still works and is safe, we ignore it. If you or a member of your family are not good drivers, then you may wish to take a more conservative (i.e., expensive) approach to your car insurance.

Strategy: I have always kept a high deductible for my family’s situation. Starting with $500 when I was young, I quickly pushed it to $1000, and then to $2500 over the last 11 years. For our cars older than 6 years, we dropped collision and comprehensive altogether even with teenagers driving as we saw they were capable, smart drivers and we could afford self-insurance. I never buy extended warranties (or undercoating) for cars.

Product warranties and extended warranties

For numerous purchases such as TVs, computers, printers, blenders, appliances, phones, etc. etc., stores (online or brick-and-mortar) often ask me if I wish to purchase an extended warranty. I never do. I also never buy coverage for repairs or replacement caused by human error. I couldn’t afford them when I was poor and I could afford to self-insure when I wasn’t. Turning down hundreds of warranty offers over the last 30 years easily saved me $10K or more (excluding investment returns). While spending the $1,000 to replace my water-damaged laptop was a bummer, it was a bargain when compared to my self-insurance savings!

Strategy: Many products come with manufacturer warranties (if they don’t I am wary, and I’ll look for a better product). In addition, I make purchases using a credit card that provides one year of extended coverage (and I get travel points), though I have never needed to make a claim. I protect my purchases, too, with physical forms of insurance–for example, I buy quality phone cases and screen covers and connect my home electronics to surge protectors.

Travel Insurance

I have found travel insurance to be the least useful insurance product for the cost. I purchased Amtrak tickets recently. With the company, I could pay $24 per ticket for non-refundable (my fault not Amtrak’s) or $26 per ticket for fully refundable and changeable tickets. While $2 doesn’t seem like much, that same rate of insurance for a $1,000 airline ticket would be $83! Then, I was offered to purchase trip insurance for $4.50 – even for the fully refundable tickets!

Most situations for travel delays like weather are covered by the airline or hotel. I have been on many flights that were delayed or cancelled and every time the airline has put me on another flight. On a trip to Hawaii, our whole family was delayed a full day and the airline paid for hotel, transportation, and food vouchers and we flew out the next day. Travel insurance wouldn’t have covered any lost wages from the delay. If a hotel can’t accommodate me, then I have always received my money back. Airlines are required to reimburse for lost luggage and in many situations for significant flight delays.

So, what if I can’t make the flight or get to the hotel? People often think travel insurance covers absolutely every risk you may encounter while traveling. It doesn’t. With all of the fine print and legal clauses, It is unusual to qualify for a travel insurance claim. For example, if I had a very specific risk, such as sudden need for cancer treatments, most travel insurance policies won’t cover the situation if it is a pre-existing medical condition. I had one friend who claimed on travel insurance during the COVID-19 pandemic. After an arduous claim process, the airline did reimburse her for the $580 discount ticket she purchased, but it didn’t pay for the $1,200 last minute replacement ticket she needed.

Strategy: I rarely purchase travel insurance. I mostly book accommodations with free cancellation (i.e. they often don’t charge extra to cancel). I use my travel credit card that provides travel insurance coverage to include rental car insurance coverage (I never buy rental car insurance coverage and I fill up before returning the car). I get 3x travel points and the same or better travel insurance coverage. In most cases where a travel change is out of my control (and often when it is), the airline, hotel, or other company will accommodate my change request. I have saved tens of thousands on cost avoidance from not buying travel insurance products!

Home Insurance

Similar to my auto insurance, I carry a high deductible on the two houses I own (currently 1% of the house replacement value). I self-insure for minor damage (e.g., small roof repair) avoiding adding to my claim history (and increased insurance premiums). If I do have a major repair that well exceeds my deductible, then insurance will be there to cover it (as it should). Since owning houses since 2004 (two since 2008), I have saved approximately $300 per house per year and I have only paid one $2,500 deductible in that time and one $1,200 claimable roof repair out of pocket. That is a savings of over $11K (excluding investment returns).

Renters Insurance

I only purchase renter’s insurance when a landlord or umbrella insurance policy requires it, and then I purchase only the minimum required liability coverage. I self-insure for the rest.

Self-Insurance Is Cost Avoidance

While my large workforce of fire-fighting emergency fund dollars are invested in a low risk investment ready to handle my unforeseen emergency expenses, they are also doing great work saving me a ton of money through self-insurance. This cost avoidance has helped me achieve financial independence and early retirement. How is your insurance strategy helping you reach your goals?