I used to be a cyclist, gardener, canner, aspiring musician, soccer coach, coin collector, stamp collector, home owner, DIY handyman, and Department of Defense hospitality expert.

I am no longer those things. I found that by selling, giving away, or otherwise disposing of my guitars, soccer gear, biking gear, coin and stamp collections, work files, house, and many, many, other possessions related to these pursuits, I was freed from the personas that took away my time and focus from the things that I wanted to be and do the most.

In his time management book Four Thousand Weeks: Time Management for Mortals, Oliver Burkman challenges us to focus on our top priorities. He shares a story attributed to Warren Buffet, in which the billionaire advises us to make a list of our top 25 priorities, then focus on the top 5 only, actively avoiding the remaining 20 items. Those items prevent us from spending the time needed to do our highest priorities very well.

Burkman himself is not this prescriptive. He explains, “You needn’t embrace the specific practice of listing out your goals (I don’t, personally) to appreciate the underlying point, which is that in a world of too many big rocks, it’s the moderately appealing ones—the fairly interesting job opportunity, the semi-enjoyable friendship—on which a finite life can come to grief.”

This concept was an eye-opening revelation for me. In order to focus on what I wanted to be and do the most, I needed to eliminate my lower priorities. In my case, that meant retiring my many appealing personas listed above, and focusing on the ones that are core for me: husband, father, friend, traveler, camper/hiker, personal finance coach, and lifelong student. Since one of my top priorities was to travel the world nomadically with just a carry-on and a backpack, I needed to do some major downsizing. I fully embraced minimalism with some surprising results.

But this downsizing is a lot easier said than done. For me, it was a long process. I truly enjoyed learning to play an instrument, gardening, and coaching soccer. To give up the things that went along with those pursuits wasn’t just getting rid of stuff I no longer valued. I was giving up valuable, but lower priority, pursuits that were preventing me from fully doing what I valued the most.

The hardest things for me to let go of were my electric guitar, amp, and case, the accessories of my dream of learning to play the guitar. I had wanted to play classic rock tunes around a campfire. On two separate occasions, I took weekly lessons for months on end. I practiced a lot, though not enough, since my identity as a musician wasn’t one of my top pursuits (and it had so much competition from my other middling-priority identities). During my second set of lessons, I spent over a $1,000 upgrading my $80 acoustic guitar for a new electric guitar and amp, thinking better equipment would help me learn quicker (it didn’t). I made small progress but not really enough to be satisfying.

After I stopped taking lessons and practicing, the new guitar remained a constant guilty reminder of the time and money I had sunk into learning to play. When I sold my (lightly used) electric guitar, amp, and case back to the music store I bought it from (at a fraction of the price), I felt free! I was giving myself permission to no longer strive to be a musician. I no longer had this physical reminder scolding me “You should practice music. Remember, it is the seventh most important thing you want to accomplish!” It was a conversation with stuff that I didn’t want to have any more.

The time and money I spent trying to learn to play the guitar took time away from what I really wanted to do—read, travel, learn a language, and take better care of myself. Likewise, by getting rid of my canning equipment, lawn care equipment, tools, old files, old collections, job (I retired early), cars, and house, I released myself from numerous commitments and freed up enormous time and resources. (Asking myself tough questions helped me change my relationship with what I owned).

Because camping is one of my top priorities, I kept my camping gear (tent, sleeping bags, inflatable mattress, and cookware) neatly stored in my friend’s basement near Seattle. These possessions support my top values as each summer I return to the beautiful Pacific Northwest and enjoy weeks of camping among the evergreens.

Enjoying our camping gear

Each person’s top priorities will likely be much different than mine, and of course top priorities can certainly change over time. When my life of traveling winds down, I may decide to return to a house and gardening or maybe pick up the harmonica.

It’s a useful exercise to distinguish your most important pursuits from the lower priority pursuits getting in your way. You may decide that learning a musical instrument is your top priority, so you’ll get that dusty guitar out of the basement and give it pride of place (and time and money) in your newly cleaned living space. You might ditch the tent that I decided to keep. The key is to hone in on your own top priorities, keep the few items that help you in those limited pursuits, and discard all the possessions that are part of lower-priority pursuits.

Having newfound time and resources to focus on world traveling, my relationships, reading, sleeping, stretching, and hiking has been amazing. I have traveled more this year (2024) than any other year. I have read more books this year than any other, including my years in college. I have spent more meaningful hours with my close family and friends than I had before embracing minimalism, because I had a clearer focus on why they were important to me. I walk and hike more than ever. I am constantly learning new things and tackling my foreign language proficiency goal.

I have swapped the elusive pursuit of happiness with the pursuit of contentment because I found that “enough” is fulfilling—enough in what I have, enough in what I do, and enough in who I am.

Doing fewer things better is…better! Removing the physical possessions around these lower-priority identities made it happen. By getting rid of these possessions, I gave myself permission to focus on the core of who I really wanted to be. Minimalism changed who I was.

[This post was republished on the minimalism and simple living website No Sidebar]

I thought my wife and I were doing everything right to achieve a rich, free life. Avoid debt – check! Spend less than we earn – check! Invest the surplus – check! So, after almost two decades of investing, why weren’t we rich or at least well on our way?

This essay is published in J.L. Collins new book Pathfinders (Harriman House publishing) — a follow-on book to The Simple Path to Wealth capturing personal stories of people who applied the many financial concepts from the book. Pathfinders is available on Amazon and other places where books are sold.

When I calculated our net worth 19 years after we started investing, we had invested $103K in principal into IRAs but their value was only $92K. We had actually lost money! I had also lost $15K out of $50K invested in a taxable mutual fund account and all of the $5K invested in individual stocks.

I thought I had done my homework. I had read an investment book, read several articles on investing, and sought advice from friends, but it wasn’t until I read J.L. Collins’ book The Simple Path to Wealth that I finally understood that my investing problem was…me.

I have been frugal and a great saver my whole life but, as you can tell already, I was a terrible investor. J.L.’s description of the “typical investor”– who panics and sells when the market takes a tumble, waiting to reinvest cautiously long after the market recovers – described me perfectly.

In 1992, when I was a young lieutenant in the US Air Force, I understood that investing in stocks for the long term was the path to financial success. My wife and I each opened a traditional IRA (this was before Roth IRAs) and invested in mutual funds.

With monthly automatic purchases, we invested the annual limit and put the rest in a savings account. After 5 years, our $17K invested had grown to over $90K and our savings was over $90k. So far so good, right? But, then along comes yours truly. Here are the most egregious examples of my rocky investing.

Individual Stock Picking Fail

In 1997, I purchased 1,000 shares of Boston Chicken (later known as Boston Market). We had recently lived in Boston and I loved our nearby Boston Chicken restaurant. I was convinced that home meal replacement was a growing trend and thus a great investment.

Unfortunately, the company was cooking more than delicious chicken. Just weeks before I purchased the stock (and unbeknownst to me), the company revealed it was recycling money by loaning to its franchisees to build new restaurants, masking its true, troubling financial picture–huge debt.

Boston Chicken soon filed for bankruptcy. I watched that stock drop from around $5 per share to pennies as the company financially collapsed. Believing that I simply needed to learn more about stock investing, I read The Motley Fool Investment Guide. It was no fun to read their take that delicious chicken does not necessarily make a great investment. I learned picking individual stocks can be very risky.

Buy High, Sell Low?

Not to be deterred, I continued to closely watch the markets for three years, saw their year-over-year gains, and thought: We can’t miss out on the tech stock boom any longer. So, in January 2000, after the Y2K scare passed but right before the dot.com bubble burst, I invested a quarter of our net worth ($50K) into mutual funds (half in a tech fund and half in an S&P 500 index fund).

Yep, I bought high, joining the excitement of a hot market. But the value of my shares burst along with the bubble. I held them for a measly four years, and when there was little to no recovery, I sold our shares, locking in a $15K loss.

I didn’t yet understand how to hold and wait for recovery. In fact, many of the remaining companies, such as Amazon and eBay, would eventually fully recover and make a lot of money. Sigh. Luckily, we left alone our only remaining investments–our IRAs–and they continued to grow… until the Great Recession hit.

In September 2008, when the Great Recession was in full swing and the stock market was way down, I convinced myself and my wife that we needed to pull our IRA investments to safety and avoid further “losses.” So with much angst, I transferred our IRAs into money market funds and locked in losses of approximately 25% percent each.

The recession made me wary of the market, so I kept our investments in money market accounts until February 2014, when I felt I couldn’t let the market rise without us any longer. By then, the market had long recovered, but my jitters remained. I was certain (as were many pundits) that the market would once again drop.

There Has to Be a Better Way

Finally, in early 2018, I found the Financial Independence movement and took on a new perspective of how to build our financial future. I discovered J.L. Collins on the ChooseFI podcast. I checked out The Simple Path to Wealth from my local library and read it from cover to cover. I gave it to my wife. I bought copies to share with my kids and friends.

Reading the book felt like J.L. was speaking to me directly, as if he knew me personally and my poor investing history. His approach is so simple, yet it eluded me for years. Armed with J.L.’s wise words (we began to think of him as “Uncle J.L.”), I now understood the importance of investing in broad-based index funds, paying low investment fees, and giving like a billionaire. But most importantly, I learned how to hold (and even buy) when the market is falling and sell (rebalance) when it is up.

Testing My New Resolve

My first big test was in March 2020 when the COVID-19 pandemic hit and the market plummeted. In the past, I would have pulled out my money after it dropped precipitously, but now I had Uncle J.L. over my shoulder reassuring me to stay the course.

I didn’t sell. In fact, I confidently optimized our available investment dollars and shifted into more stock. I now trusted that, eventually, the market would rise again.

In early January 2022, I rebalanced our portfolio, selling stocks at their peak and buying government securities (I needed to wait on bonds as interest rates were rising). In early June 2022, when the market dropped 15%, I shifted funds from government securities to buy stocks “on sale.”

When it further dropped into bear market territory, I purchased more stocks at a deeper discount. If it drops past 25% or even 30%, I’ll do it again. Since reading The Simple Path, our stock portfolio has increased by 60% and we have achieved financial independence.

I am no longer investing with angst and a trail of lost opportunities. Now, my wife and I are investing thoughtfully, our eyes on the horizon, confident the market will eventually recover. Our two children, both in their early 20s, are getting a great start to a lifetime of smart investing. Thanks, Uncle J.L.

I have noticed a trend in personal finance circles distorting the concept of the “latté factor” which I mentioned in my article “Has the FIRE Movement Lost Its Way?” but I believe needs to be addressed directly.

As a quick primer, the latté factor was made popular by personal finance author David Bach in his book The Latté Factor. In basic terms he outlines the latté factor as changing our spending behavior on small frequent purchases like a daily coffee and instead investing that money. By doing so, these small savings will add up over time and make a difference in our financial future through the power of compounding. But his book is definitely not just about coffee. It is about controlling all of the seemingly small frequent purchases in order to buy your financial freedom—true control of your time and resources.

However, on recent personal finance podcasts and in blogs, hosts and guests are frequently saying that you don’t need to give up your daily coffee to achieve financial independence. For example, on a recent back-to-basics episode of ChooseFI (one of my favorite personal finance podcasts), host Brad Barrett and his guest Jackie Cummings Koski discuss the importance of frugality. While they talked about “the value of small changes” by saving money on subscriptions, cell-phone plans, and insurance, they gave a pass to buying a daily latté. “If you need your coffee, then you should buy that,” Brad says. Why not save on coffee too? I suspect it may have something to do with financial author Ramit Sethi’s strong stance against cutting out lattés, which Brad has mentioned in the past.

Advice to reduce monthly cell phone bills but give a pass to daily latté purchases sends a confusing message to those trying to establish good spending habits. Making frugal decisions in the pursuit of financial independence includes examining all of our small (and large) habitual purchases, especially those that could be replicated in a more affordable way, like our daily coffee purchases. Here are my 4 reasons why our daily coffee purchase should be included in back-to-basics money advice.

Reason 1: You don’t have to give up your daily quality coffee.

This is probably the biggest distortion. Not paying $5.50 a day for coffee does not mean we can’t get our coffee fix. We can make a fabulous cup of coffee at home for a lot less and in the same or less amount of time than buying a coffee out. This includes a quality coffee maker, good beans, your favorite milk, and any specialty seasonings you like. (When thinking about time spent buying a coffee out—driving there, ordering, waiting, and driving on—don’t forget to count the time you spend at work making the extra after-tax money to pay for it).

Reason 2: Forgoing small habitual spending matters to financial success.

Does replacing our daily latté purchase with a homebrew matter to our financial success? Yes! As outlined in this article from The Perky Kitchen blog, we can save ~$4.30 on each latte we make at home (the author included the cost for a latté machine depreciated over 3 years—a conservative estimate). Since coffee is almost always a daily habit (thanks caffeine), avoiding paying $5.50 per cup 24 times in a month and paying $1.20 instead will reduce monthly expenses by $100 ($130 if it is truly a daily buy-out habit) AND we still get to have a delicious cup of custom made coffee at home! The elusive win-win.

In the aforementioned ChooseFI episode, Brad explained that reducing expenses by $100 a month reduces our financial independence number by $30K! And, by investing that money over 20 years at an 8% average return will add $60K to your net worth—a $90K swing! Yeah, it matters!

Reason 3: More important than saving money is positively changing our financial habits.

You might be asking, why are you picking on coffee, anyway? Simply put, coffee provides a great example for controlling spending—it is popular (i.e., applies to most people), it is usually a daily morning habit, it is often bought out, and while it seems like an insignificant expenditure, it quickly adds up. But most importantly, it is a habit that hits early in the day, setting the tone for the rest of the day. By making our coffee at home, we are making a positive financial decision first thing in the morning, powerfully reinforcing our goal of financial freedom. By starting our day off on the right foot, we set ourselves up for other positive financial decisions later. More important than the actual monetary savings is the positive change to our financial habits—good habits are powerful!

It is definitely not just about coffee. We need to examine all areas of spending, large and small, where we make financial decisions out of habit or without thinking about their impact on our overall budget. Doing so will help us identify areas where we can implement positive financial habits.

Reason 4: Making your own coffee builds skills, self-reliance, and self-confidence.

Skills are assets! Making a quality latté is a skill. Doing foam art is a skill. When we do things for ourselves we learn new skills and accomplish things which in turn builds our self-reliance and self-confidence. This self-confidence helps us tackle bigger projects which instill more self confidence and sense of accomplishment—a virtuous cycle.

My 25 year-old son is a great example. About a year ago, he started drinking coffee on a regular basis. Instead of joining the crowds at Starbucks each morning, he taught himself about coffee. He learned about quality beans, roasting techniques, grinding, and how to make espressos, cappuccinos, and lattés. He invested in a high-quality at-home espresso machine, and found a local roaster that he likes. He not only has an exceptional cup of coffee every morning for a fraction of the long-term costs, he has coffee skills. He can converse deeply with fellow coffee nerds and offer his guests an exceptional custom-made cup of joe complete with foam art. Now instead of heading to the coffee shop when we visit, my wife and I enjoy a relaxing morning at his place.

My son enjoying his high-quality cup of coffee at home (complete with foam art)

Making our own coffee is empowering, as is making our own lunch and hosting friends for a drink on our patio. I offer some examples from my life on how I am able to get the same basic goods or services for a lot less money in this article on how frugality made my life happier.

Some final thoughts.

Making coffee at home or any frugal practice isn’t an all-or-nothing proposition. We can still meet a friend at a coffee shop for a coffee (and confirm if your home brew skills are outpacing the competition), or have a drink out, or eat out occasionally. A single $5.50 expense won’t break the budget and an occasional break from the routine won’t destroy our good financial habits. In many cases, we will be reminded that our coffee and cooking is better anyway. I have learned that it is not spending more that makes me happier and more content, it is primarily spending quality time with my family and friends, time in nature, learning, and taking care of my health that brings the most happiness—all of which can be done without spending a lot more money.

The latté factor is most important when you are starting on your financial journey.The financial experts who disregard the latté factor may have forgotten what it is like to get started on the road to financial freedom. Ramit Sethi’s advice to just put away 10-20 percent of your money into savings first and then not worry about how you spend the rest (to include your daily latté if that is your desire) breaks down under scrutiny. For people living paycheck-to-paycheck, there isn’t 10% readily available. In many cases people are paying off credit card debt trying to get back to zero. Investing a thousand dollars in the stock market making 12% is a losing battle against carrying a thousand dollar credit card balance at 23% interest. Financial advice needs to meet people where they are!

Ramit also advises to focus on the big expenses like housing, cars, and education expenses. To make any progress, we have to spend less than we earn. Day one of our new financial life starts with controlling our spending. The first thing we purchase is likely our morning coffee. Of course, we also need to look at our big expenses like housing, transportation, and food, but $100 in coffee spending each month matters, as does spending on subscriptions, drinks out, etc. It’s not big expenditures or small ones—it’s both. But it usually starts with controlling the small habitual purchases and freeing up those 5s, 10s, and 100s in the budget which can quickly add up.

After we have our consumer debt paid off, a solid emergency fund, a sizable amount in investments and strong financial habits in place, then we can worry a bit less about the smaller purchases. They become less and less material the stronger our financial picture grows. At that point, we can buy out our coffee every day if we want to…but will we want to? When we’ve got a system for great coffee at home?

Let’s not ignore or distort the power of the latté factor when we are talking back-to-basics of personal finance. Coffee anyone?

We can learn to make our own delicious cup of coffee and enjoy it in our favorite mug in the comfort of our own home for a fraction of the cost of buying a coffee out.

My dad was a “jack of all trades,” and there was little he couldn’t do himself. He made his own soap, handmade moccasins from a bear hide he tanned himself, reupholstered furniture, built a barn, a double-axle trailer (did all his own welding), laid bricks, rebuilt a carburetor, kept bees, added a bedroom and bath to our house (and did all his own plumbing and electrical), installed a wood-burning stove, and then built an entirely new house for his retirement years. During the high unemployment of the early 80s, my dad was laid off from the logging industry in our depressed rural county for over a year and a half, but he was able to do piecemeal handyman work, sell firewood, keep a garden, and hunt to keep food on our table until he was able to find steady employment again.

[Cover Photo Caption: Building a fence at one of our rental houses. Our landlord was so impressed he paid me $500 for the fence when we moved out!]

I was his (often involuntary) helper. I remember holding a light very still for what seemed like hours (but was probably only 20 minutes) in the freezing cold under the car at night while he repaired it. And though I was sometimes reluctant in these adventures, I absorbed a lot. His example taught me about self sufficiency and the importance of having a broad base of skills.

Helping my Dad build a table—he let me sand the top. He was always making something. (I loved that hat!)

Skills are assets. While they don’t show up on our net worth tracking spreadsheets (maybe they should?), they represent future value to us in terms of cost avoidance, self reliance, and accomplishment. Each time we learn a new skill and use it, we increase our net worth. So often we blindly just pay other people to do things for us that we could do ourselves and increase our skill-based assets. Here are six reasons for doing things ourselves instead of hiring out the job.

Reason 1: Skills save money (cost avoidance).

When we think about do-it-yourself (DIY), we often think about saving money. DIY is spending some of our time doing or making something instead of paying someone else a lot more to do it or make it for us. For example, when Launa and I bought our house in Virginia, we needed a shed for our bikes, lawnmower, and other tools. Instead of paying $6,000 for a new shed delivered to our house, my father-in-law (Pop) and I built one ourselves. For less than $800 in materials, I had a 8’x12’ shed (inside dimensions) with windows, a double-wide door, and attic space. If I counted the $1300 in net salary lost for the hours I spent building it (which I don’t, as I’ll explain later), I still saved almost $4,000!

Building a shed with Pop. He helped me with many projects over the years (to include replacing my car’s timing chain belt and water pump in college when I was broke). As a mentor, he also taught me a lot about self reliance and self confidence.

My wife and I DIY our trip planning and we save a lot of money doing so. For example, when we hiked inn-to-inn along Hadrian’s Wall in England, we paid $1600 (56%) less than we would have if we booked the same trip through a popular tour operator. That’s good pay for about two days of work! But we also got a trip tailored to our exact preferences, we stayed closer to the wall some nights than the tour would have arranged, AND we gained a deep knowledge of the trail which enhanced our hike. We enjoyed similar savings by planning our trips along the Via Degli Dei in Italy, the Lycian Way in Türkiye, and the Archipelago Trail in Finland.

But DIY isn’t just about saving money. It provides numerous other benefits even in cases where it costs a little more than paying to have it done by someone else.

Reason 2: New skills keep us learning.

Life-long learning has a positive impact on our mental health and well being. Instead of spending our free time on passive activities like binging TV series, we can engage in activities that teach us new skills. DIY, baby!

DIY is project-based learning. Building that shed with Pop taught me a lot about construction. I learned how to frame out the walls, design the barn-style roof, install windows and doors, and shingle the roof. Little of that I knew how to do before we started, but we figured it out.

Over the years I have learned basic electrical and plumbing work, drywall repair, computer programming, property management, personal finance, gardening, canning, and appliance repair to name just a few. The learning and problem solving inherent in DIY projects is great for my brain and provides an outlet for my creativity.

Building a tree house with Pop. This was a fun project to design and build together.

Reason 3: Learning skills instills self reliance.

While saving money is great, skills provide flexibility and value in a changing world. This idea was well expressed by Jacob Lund Fisker in his book Early Retirement Extreme, where a primary goal of his was to break free of the work-buy-work cycle and learn to do things himself. By having a multitude of skills, we can weather unpredictable changes in employment (like my Dad did), our health, prices, and the supply chain.

By being more self reliant, I don’t have to pay higher prices. I can skip a long wait for a car repair appointment or for a contractor to fit me in. I can get things done on my own timeline.

My prized jalapeños—tasted much better than store bought. I learned to garden (I grew the jalapeños and dill), can and dehydrate foods, fish, and hunt. (Yes, that is a G&T to celebrate).

Reason 4: Skills save time (usually).

It might sound counterintuitive, but many times doing something yourself can save time over hiring someone else to do it. For example, when the side mirror on our car was broken off by a passing car, I could have called around for quotes, scheduled an appointment, drove the car across town to the shop and then either waited a few hours for the repair work to be completed or had my spouse pick me up and bring me back, THEN paid for the repair, drove home, AND worked 12.5 additional hours to pay the cost difference from doing the repair myself.

Instead, this is what I did: I quickly searched online for aftermarket parts, ordered the mirror to fit my car, reviewed the repair tutorial video provided by the parts website, bought the $11 door-cover-remover tool at the nearby auto parts store, and followed the video tutorial to replace the mirror and test it. It worked great! In a total of 2.5 hours I did myself what paying someone else would have taken 15 hours or more of my time. Even if, for example, my salary was twice the national average, it would still take 9 hours to pay for it! So while it might seem like paying someone else to do something for us will save time, it often takes more time than doing it ourselves—what I call “the tyranny of convenience.”

Not to mention, I was really proud of being able to do it myself which leads me to…

Reason 5: Skills reward us.

Repairing my refrigerator, building a shed, replacing a bathroom sink, and patching drywall is extremely rewarding. I enjoy the process of learning how to do something and then exercising those skills and seeing the tangible results. Every time I complete a DIY project I have a great sense of accomplishment and take pride in knowing that I was able to figure it out myself. As I write this post, just thinking back over the many projects I have completed fills me with joy. I don’t feel that joy when I pay someone else a lot of money to do the work for me.

DIY renovation of narrow kitchen pocket door into an archway before (left) and after (right). We enjoyed our kitchen and living room space far more with this change (and I suspect made our house more valuable).

Reason 6: Skills build self confidence.

On top of a sense of accomplishment and enjoyment I get from DIY projects, I also garner more self confidence. The more I am able to do myself, the more confident I am that I can tackle more complex projects. I didn’t start with building a shed. I started with hanging pictures and replacing furnace filters. Then I progressed to replacing door knobs and repairing lamps switches which progressed into minor drywall, electrical, and plumbing work. The more skills I learned, the more confident I became to tackle increasingly complex projects.

How can you build your DIY skill set?

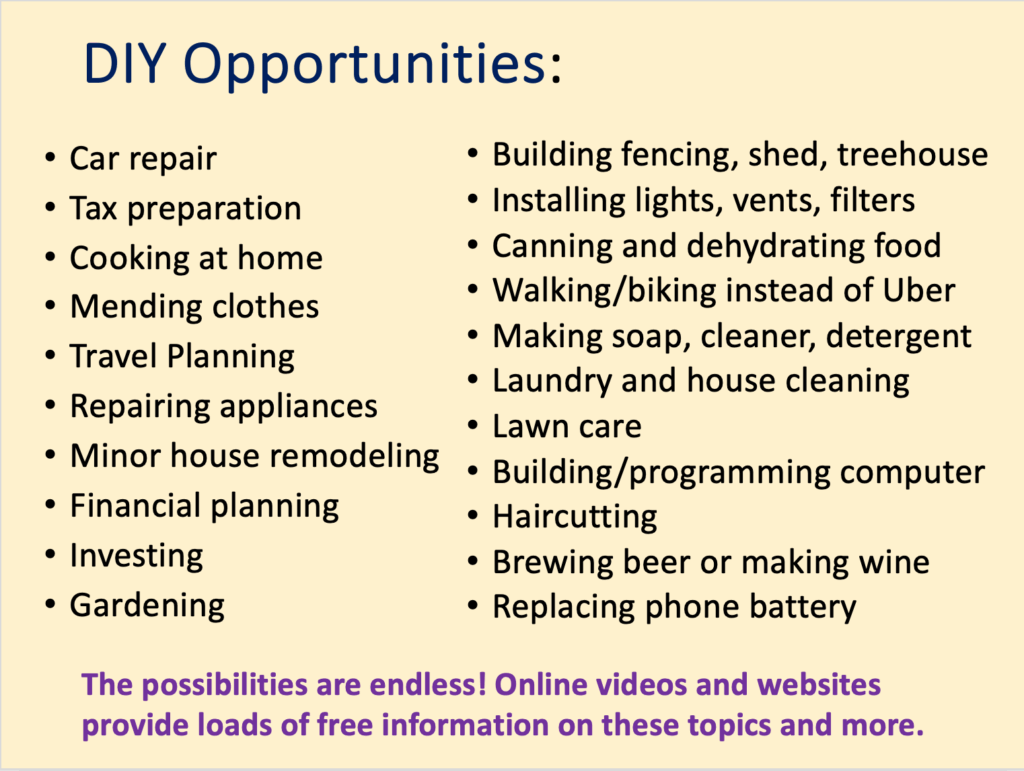

DIY isn’t just house repairs or fixing your own car. It is doing anything that we might hire someone else to do for us to include taxes, investing, moving, travel planning, rental property management, gardening, yard maintenance, making coffee, and cooking. It can also be more abstract skills like walking or biking instead of taking an Uber, learning to exercise and eat well, or doing a home exchange instead of purchasing lodging on vacation. Here is a list of some DIY opportunities to help you brainstorm:

I ran out of room on the graphic before I ran out of DIY ideas!

What skills do you already have that you could expand on? What would you like to learn how to do? Identify easy opportunities that could be quick wins to build your confidence. Maybe start with mending a hole in your favorite shirt, sewing on a button, replacing your windshield wipers, or making pizzas at home (I love my wife’s homemade pizzas!). Don’t start with something too big like replacing the brake pads on your car, as you risk being overwhelmed and losing confidence.

Tap into available resources. Search online—there is a video, website, or interest group for every type of DIY project. The wealth of online help hasn’t failed me yet!Seek out a mentor. Local groups, friends, neighbors, and relatives can be great resources. I learned a lot from my Dad, my father-in-law (Pop), and friends on how to tackle different projects. If you want to brew your own beer, I suspect someone you know can help you get started.

Some tools you’ll need can be borrowed from your library or neighbor, and many tools can be rented, too. But even if you need to buy a tool, just one DIY project will normally cover the expense, and subsequent uses make it even more cost effective. Over the past 35 years I had built up a set of tools that I frequently used to complete my DIY projects, from basics like a hammer, multipurpose screwdriver, and drill to specialty items like canning equipment, a mitre saw, and a haircutting set (my wife has cut my hair since 2006).

Take pride and celebrate your DIY wins—and that includes when a project doesn’t go to plan. You are learning new things and building a skill set, even if you need a second (or third) try, or a little help this time to get it done. My wife and I are each other’s biggest fans and support and appreciate our DIY skills. Take photos before and after and share them online and with friends, co-workers, and family. The positive feedback is energizing!

The finished shed that Pop and I built together. I’m very proud of this project! (Note my garden in front—another DIY project.)

Even after I downsized and no longer have a house, car, or many belongings, I still exercise my DIY skills. I help family and friends with projects at their houses or with financial planning. I sharpen knives at our long-stay accommodations and even do some minor repairs (I even built a bed frame for one host!).

DIY projects feel great, save money and time, help us learn things, be more self reliant and self confident, and help others.

How are you increasing your skill-based assets?

I built this frame for a long-stay AirBnB which took me about 3 hours (with the host’s approval and reimbursement for materials cost). It kept the mattress from sinking into the well of the bed frame (clearly not the right mattress for this frame). I slept much better afterwards!

Wouldn’t it be great if we had a machine that would save us the trouble of hanging up our clothes on a line to dry? No more waiting numerous hours, often overnight, before the clothes are dry and ready to fold and put away?

We could save that time with the right machine. All we’d have to do is take the bundle of wet clothes from the washing machine and plop it into this brilliant new machine, scrape out a small sock’s worth of lint from the previous load, close the door, choose from 12+ settings, and press start.

Dried clothes in 40 minutes—hot dog!

Well, that’s after I separated my cottons from my synthetics, from my delicates, from my (hypothetical) cashmere (which I have to line dry anyway). So they all couldn’t dry at the same time. But still…amazing idea, right?

I would need to drop $700 on this new-fangled machine and spend another $525-$750 annually on electricity. Plus an average of ~$60 per year on repairs, and then buy a replacement machine in 10-13 years. But what else would I do with $730 a year? At the average American’s $24 per hour net wage, that is only 30 hours of extra work per year—just 35 minutes per week. Nothing…right? Have I mentioned I would save 20 minutes hanging up my clothes to dry each week?

Don’t forget I would need to purchase replacement clothes much more frequently as that large clump of lint each load takes its toll—clothing fibers break down more quickly and my clothes get holes more quickly. But hey, that’s a great excuse to buy new stuff!

And I haven’t mentioned yet the ecological impact of building the machine, generating the electricity, and making the extra replacement clothing. But what would my kids and grandkids want with all those natural resources anyway? I saved 20 minutes!

Well, maybe electric clothes dryers aren’t the indispensable appliances of modern households I thought they were. The “convenience” they deliver comes at a high price—tyranny of convenience. But it’s not just dryers.

Over the decades we have been sold machine after machine with the promise to make our lives more convenient. From washers and dryers, to dishwashers, to microwaves, to cell phones, to robot vacuums. We’ve also been sold service after service, such as next-day (hour?) shopping delivery, food delivery, instant communication, music and entertainment services, and on and on.

Most conveniences come with a price. They often cost more money, but also cost us in terms of what we value—time, contentment, happiness, environmental impacts, self-reliance, and in-person human interactions.

Were we less happy in the 70’s before microwaves? Or in the 00’s before smartphones were in every pocket? We didn’t become less busy people with the addition of each convenience. How much of our newly freed-up time was spent earning the money to pay for these conveniences?

Do we work fewer hours now that we have a computer on every desk? I certainly didn’t, but instead of talking with people in person, I wrote and responded to emails. The convenience of my computer and email was at the cost of direct human interaction. The job still got done, but it was far less enjoyable.

So many aspects of our lives are driven by the allure of convenience, but at what cost?

Does online shopping save us time and money? Or do we actually buy more than we need on high-interest credit cards because it is so convenient?

Are the 15 minutes we save from picking-up our food from the restaurant worth the extra hour we have to work to pay for it? Is it worth the lukewarm and soggy product we so often receive?

Are food delivery robots worth the convenience? (Outside “convenience” store in Turku, Finland)

Conveniences often cost us more than we realize—a Faustian bargain.

“Faustian bargains are by their nature tragic or self-defeating for the person who makes them, because what is surrendered is ultimately far more valuable than what is obtained, whether or not the bargainer appreciates that fact.” — Encyclopedia Britannica (online)

Many conveniences cost more than the alternative, thereby requiring us to work longer hours to pay for them. Like my clothes dryer and food delivery examples, we try to buy back time by hiring a house cleaner or lawn service but often wind up working more hours to pay for it than the time we saved.

Many conveniences erode our self-sufficiency. Cooking, for example, is an important life skill. The convenience of eating out or buying preprepared, precooked, precut, preseasoned and prepackaged usually costs more, is often less healthy, and degrades our ability to nourish ourselves. This can be applied to laundry, cleaning, delivery, repairs, etc. Skills are assets and self-sufficiency builds our self-confidence.

Most take more resources to produce or deliver. Just drying my clothes on a simple clothesline, for example, takes far fewer of our Earth’s resources than a clothes dryer.

Many reduce our in-person human connections. We text instead of calling. We post instead of getting together in-person.

Some are actually inconvenient. Having my dentist, plumber, bank, and every business I have ever been a customer with (and many I haven’t), send me a DM or email to my phone at any time is very inconvenient.

Conveniences can also expose us to a litany of choices, which brings me to the tyranny of convenience’s evil step-sister…

The Tyranny of Choice

The convenience of having unlimited choices with convenient services such as Spotify, Amazon Prime, and food delivery services introduces the tyranny of choice where some options are good, but nearly unlimited options actually reduce our happiness. We want to listen to the perfect song, find the perfect movie for tonight, or eat something really delicious. And so we spend hours researching through endless options, weighing reviews, and comparing choices only to be less happy because our expectations were so high (it got a 4.8 with 389 reviews, so it must be great, right?). Analysis paralysis—ugh!

With so many choices in daily life, I find myself wanting fewer choices. I am happier when I have fewer media choices, when a menu has only 10 items, when a flight only has only 10-15 movies instead of 200. The more opportunities that confront us, the more opportunity costs we perceive in comparison to the choice we actually make and the less happy we tend to be with our choice (Scientific American, Dec 1, 2004).

Thinking about the conveniences we use.

Not all conveniences are problematic, and there are some ways to mitigate their negative impacts. Some save money and time and make life better and easier. Which conveniences are worth it and which ones are not will vary for each person. For me, a vacuum cleaner cleans my rugs and carpet better and quicker than I could without it, but I value the cost savings, self-reliance, and self-confidence I get from repairing my vacuum cleaner myself.

What I am suggesting is that we think about the conveniences that we rely on and evaluate them for how much they are truly adding to our lives. Then weighing that against how much they might be subtracting in costs (and hours needed to earn that money) as well as social, environmental, and other impacts.

I am not a fan of crunchy towels, but the costs of a clothes dryer far outweigh any benefits for me.

If this gondolier’s family doesn’t need a dryer, neither do I (Venice, Italy)

Five years ago, I took the leap to retire early—fifteen years before Social Security’s full-retirement age. I left my career as a civil servant at the Department of Defense at its peak—not just in terms of my highest compensation but also my greatest influence and status. And yet, it was one of the best decisions I have ever made. Since retiring early, my life has changed for the better—no regrets. Looking back on these past five years, here are eight things I learned about early retirement and myself:

[Post Photo Caption: Immersing myself in history at the Giza complex in Egyptas a full-time traveler]

Lesson 1: You don’t have to have your retirement figured out before you retire.

You really don’t. I wrote about this in my post on myths of early retirement, but it deserves some additional explanation as I received some feedback. When I retired, I had a general idea that I wanted to follow my curiosities and no longer spend the majority of my waking time and my physical and mental energy earning more money than I needed. When I left my full-time job, I had no idea that I would become a minimalist, find my dream job, quit that job, and travel the world full-time for two years and counting. I didn’t know how I or my retirement would evolve before I retired, and I didn’t need to know, yet. That knowledge unfolded.

When you or I retire, we don’t mysteriously become another person. Our minds don’t turn to mush and we are only saved by careful retirement preparation, planning, and practice. Instead, we wake up the next morning like we would on a long weekend or vacation (hopefully without an alarm) refreshed and ready to tackle the next chapter of our lives to include figuring out what that chapter will look like. I didn’t suddenly stop being a doer and lose any sense of my ability to learn things and get things done. Quite the opposite. I now had ample time and a full tank of physical and mental energy that until now I’d been applying toward work to apply toward figuring out retirement.

Before retirement, when I was physically and mentally exhausted working long hours at my job and fitting in my everyday life chores around that, was not the right time to try out new hobbies or make new retirement friends. Forcing a new hobby into my already busy life and precious little down time, particularly one that would benefit from daytime hours and my full energy, would have added to my stress and risk me resenting the new endeavor that I might otherwise enjoy.

It is OK to not know what you want to do in retirement. Leaving work frees up the time and energy to explore and try out new things and meet new people. I learned an enormous amount about myself after retirement because I had the time, energy, and resources to do so. We don’t have to have it all figured out in advance—we can leverage our time in retirement to do just that. Protect what little white space you have in your working life and know that retirement will provide ample time to decide what to do next.

Lesson 2: Stress testing your retirement plan works.

Stress testing my wife’s and my retirement plan has paid big dividends in how well we are enjoying our retirement. It made us both comfortable to retire early and brought comfort and confidence as our plans in retirement have evolved significantly over the last 5 years.

Stress testing isn’t just calculating our safe withdrawal rate that our investments would provide and comparing that to our known expenses. I also stress tested our retirement plan against unforeseen life changes that might derail our plan, such as one of us dying early, divorce, long-term care needs, or major health challenges. We also tested our plan against increased spending on family and favorite charities beyond our planned retirement spending levels.

Due to this stress testing, handling a surprise major health diagnosis a year into retirement didn’t derail our plans. Similarly, increasing our financial support of our family and donating more to causes we value hasn’t altered our plan. Stress testing our plan helped ensure our successful retirement. I provide more details on stress testing my retirement plan here.

Lesson 3: Trusting your retirement plan is key to enjoying retirement.

There is an important mental component to overcome when retiring early—fear. Fear that inflation will skyrocket, fear that the stock market will tank for an extended period, and fear that we missed planning for some unknown expense that will derail our retirement. I learned that this fear is unfounded. The 4% safe withdrawal rate that underpins financial independence is already very conservative and includes historical fluctuations in inflation. All of my double checking of spreadsheet formulas, running performance scenarios, and stress testing our plan made our plan even more solid. I had to remind myself that we have a lot of flexibility to adjust spending which creates options in our plan. My fear was self-imposed and unfounded, and by recognizing it, letting it go, and trusting my plan, I greatly increased my contentment with my choice to retire early.

Lesson 4: Work identity is a self-imposed weight.

Our identity is frequently intertwined with our jobs. In the US, asking what you do for a living is a common first question when meeting someone new. As a society, we put a lot of weight on our work and measure our importance by our titles. I was no different. I was proud to tell people I was an Air Force officer for 20 years, then a civilian director at the Pentagon after that.

So when I decided to retire early, I was worried about what I would tell people when they asked what I was going to do after leaving my job. A significant reason I decided to become a graduate student after retiring was to be able to tell people at my old job that I was going back to school full time, as they (and I) struggled to understand my decision to leave my hard-won director’s position. I thought “grad studies” carried a level of respect and fit within society’s paradigm of what I should be doing with my time. Telling people I was “retired” sounded less important and I assumed people would think less of me. But the truth is, all of the weight and importance of a work identity was self-imposed. When I let that go, I was better able to discover who I really was—what was most important to me.

When I left graduate school, I decided to own my early retirement and just tell people that I was retired. I discovered that people didn’t care (many were intrigued) and the importance of the title was really about my own judgment of myself.

Our identities should not be primarily defined by our jobs. My identity consists of many things. I am a husband, father, brother, son, and friend. I am a traveler, reader, hiker, minimalist, language learner, coach, student of history and of life, and writer. Who I am has changed over time and I will continue to evolve. By recognizing the power and weight we give to our job identity, we can put it into perspective with all of our other identities and help us mentally transition to early retirement more smoothly. The self-imposed weight of paid work titles no longer overshadows who I really am—a proud early retiree.

My official photo when I was promoted to Director of my office at the Pentagon. It was challenging to let go of my work identity when I retired early (but not challenging to let the suit and tie go!).

Lesson 5: Even with total time freedom, you have to focus on your top values.

Since retiring I have learned to focus on what I value most. I knew beforehand I needed to focus more on my health, so that one was easier. But it took more effort to identify what I wanted to do most with my newfound time freedom. I tried graduate school to pursue my love of history, cycling, gardening, and working my dream job educating service members on personal finance. I also wanted to travel more (a lot more) and spend more quality time with my family and friends. I wanted to improve my language skills, and read more. Trying to do all of these and keep up our house, cars, yard, and other commitments meant not doing any of them very well. I found that by slicing up my time with so many activities often derailed what was most important to me.

A big step in helping me refine what I valued most was minimalism. I began a two-and-a-half-year process of letting go of everything that was holding me back. Through that, I was able to identify my top five values and actively stop doing numbers 6 through 20 that were eating up my time and energy. I discovered that the more I traveled, the more I wanted to travel. I also didn’t want to repeat my mistake of not spending enough quality time with my dad before his Alzheimer’s worsened. As I shed my possessions my clarity of what I wanted to do came into focus—lots of slow travel, more quality time with family and friends, focus on my health, reading more, and improving my language skills and history knowledge.

By letting go of my full-time job and the physical possessions around my lower value interests, I was able to focus on what was most important to me. I know my values will change over time, but the process I learned, of identifying what I value most, will remain.

Following my curiosity at the Egyptian Museum in Cairo—I spent all day there!

Lesson 6: It’s harder to transition to retirement if your partner still works.

Having time freedom as an early retiree was (is!) fantastic, but early on I didn’t have complete time flexibility as Launa (my wife and best friend) continued to work for two more years. Similarly, my other friends were working also. So, while I enjoyed riding my bike along empty trails, hiking when no one was around, visiting DC’s fabulous free museums mid-week, I didn’t get to share these experiences with my best friend and compound our memory dividends.

To mitigate this challenge, I pursued projects that helped fill my days and free up time when my wife and other friends were free. A key thing was doing shared chores like grocery shopping, laundry, dishes, car maintenance, and other errands during the day so when Launa was off work we could fully enjoy our evenings and weekends together. I spent my first year of retirement as a full-time graduate student. I completed most of my reading and writing during the day. I pivoted from grad school to personal finance coaching during my second year and worked in my dream job. But when my wife decided to retire early also, I was very motivated to align with her six months later when I quit my dream job.

For the last 2.5 years, retirement has been spectacular because we are enjoying it together with complete time freedom. While I certainly enjoyed my first 2.5 years of retirement, I was still tethered to the working world’s schedule. I learned that the benefits of early retirement can be more fully realized when your timing aligns with your partner.

Early retirement would not be nearly as sweet without my best friend to enjoy it with!

Lesson 7: Having complete time freedom is gold.

Not all time is equal. I recall when my work day was chopped into a hundred 5-minute periods responding to email, voicemails, and putting out the latest fires with leadership and my staff. Though I frequently worked long hours, I struggled to find time to tackle the most important tasks because they required hours of uninterrupted time to accomplish. I had the same amount of time each day, but it wasn’t effective time when it was chopped into small pieces and limited my options for what I was able to accomplish.

Coast FIRE: Having enough invested early in life to be able to retire in your 60s (aka coast FIRE) is better than the traditional retirement path (slowly investing 10-15 percent every year until age 67) as coast FIRE offers more flexibility of work choices to include part-time opportunities. But you will still have to work to pay the bills until retirement, so your time is not fully your own.

Barista FIRE: Having your passive income cover some of your expenses and having to work part-time to cover the rest, such as working as a barista (aka barista FIRE) also provides more flexibility than the traditional retirement path, but work still controls a portion of your schedule and limits your time options.

Sabbaticals: Taking periodic sabbaticals, either within a job or between jobs, can provide some increased time flexibility, but it is limited by the length of the sabbatical and your financial situation. For example, you cannot commit to a 2-year volunteer opportunity if you only have 3 months off. Work sabbaticals often delay achieving full financial independence by spending early savings before it can compound.

Being fully financially independent with the ability to retire early (aka traditional FIRE) provides the most time flexibility. Every hour—every day—of retirement has every possibility. You decide (not your boss) what to do with your time. It wasn’t until both my wife and I achieved full financial independence that I realized how free my time was. We can now say yes to anything and our only time limitations are those we impose on ourselves—pure gold! Knowing how much more valuable my time is now, I wouldn’t do it any other way.

Lesson 8: My previous accomplishments reduced pressure to pursue big external goals in retirement.

I recognize that the earlier one retires the harder it might be to not continue working for pay to fulfill the human need for accomplishment. I worked 30 years full-time after college. Twenty years on active duty and ten years as a civil servant at the Pentagon. My jobs focused on service to military members and their families. I am proud of all I accomplished in the working world. Also during those 30 years, I served on the board of directors for two nonprofits, served as president of the neighborhood civic association, and coached recreational soccer for 25 seasons.

I share this because I no longer feel that strong desire to “make my mark” externally as I did when I was younger. I don’t need to “find my purpose” in early retirement. My need for purpose was fulfilled with accomplishment over those 30 years. I had long strived for external validation (promotions, awards, accolades, prestige) that my jobs readily provided. Looking back, I can see that one downside of this external focus is that I had prioritized it over taking good care of my health and spending more quality time with my family.

Now as an older early retiree (I retired at age 52), I feel freer to focus on myself and my family and friends. This was something I knew was missing, but I wasn’t able to take action until after I freed myself from the inertia and gravitational pull of the working world. I have learned to focus on what I value the most, no longer trying (and often failing) to squeeze in health and family around work commitments.

Presentation of a shadow box at my retirement from active duty — the Air Force provided many opportunities for fulfilling purpose and gaining a sense of accomplishment and recognition.

My first 5 years of early retirement have been great. I trusted my plan. I shed many societal pressures related to identity and accomplishment. I learned the value of time freedom and having someone to share it with. I learned about the power of minimalism in helping me focus on what I valued most. I let myself change and I look forward to continued evolution in the next five years of early retirement.

I enjoy the work published on No Sidebar. It is one of the few blogs I regularly follow and I have been honored to have a few of my pieces published there. It has a large reach and positive influence in the minimalism and simple living community. Recently, however, I felt I needed to provide another perspective on an article titled “10 Things We’re Told Will Bring Happiness—But Rarely Do” written and published by No Sidebar on August 27, 2025, which has a short but problematic section on early retirement. I hope that this response article allows readers to consider how early retirement and happiness are intricately connected.

The No Sidebar article lists some common things that don’t deliver on their promise of happiness. It begins:

“Many of the things we’ve been told will bring us joy end up draining our time, money, and energy instead. They can keep us chasing a version of life that’s shinier on the outside than it is satisfying on the inside. Happiness, it turns out, has less to do with what we own and more to do with how we live. Here are ten things our culture says will make us happy—yet rarely do.”

Then the article lists several things that, I agree, can be hollow ways to try to find happiness, such as a popular social media profile, pursuing the latest technology, and keeping up with everyone else. But then it goes on to include early retirement on that list as something that won’t bring happiness. It says:

“Retiring early sounds appealing—until you realize that meaning and purpose aren’t guaranteed by having more free time. Happiness often comes from work that matters to us, whether paid or volunteer. The key is less about escaping work and more about finding or creating work worth doing.”

There’s a lot to unpack here. Below I identify four implied assertions these passages make about early retirement, and provide my responses to each of them.

Implied assertion 1: Our culture promotes early retirement as something that will make us happy.

Our culture is actually sending a very different message—spend, spend, spend to be happy. In fact, this same article identifies the cultural pressures we face to buy the latest stuff (items 1, 2, 5, and 9), upgrade our stuff (item 7), and keep up with the Joneses (item 10). I agree: the cultural message to not retire early and keep making (and spending) as much money as possible is a strong one. Most mainstream tax advisors recommend saving just 10-15% of your income for retirement. At that rate, most people won’t be able to retire until their 60s. That’s not a strong cultural push for early retirement.

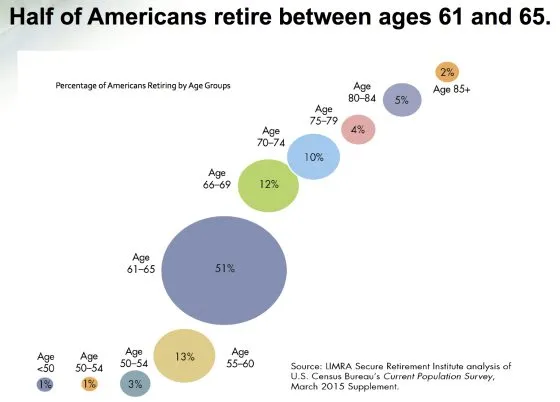

In addition to cultural messages against early retirement, there are structural barriers, too. According to the Life Insurance And Market Research Association (LIMRA) the vast majority of Americans (82%) retire after age 60 (see chart). This is not surprising since laws prevent us from collecting early Social Security until age 62, Medicare until age 65, and full Social Security until age 67. In addition, tax-deferred accounts like IRAs and 401Ks are generally penalized 10% for withdrawals before age 59.5.

It is unclear why the chart displays two “Age 50-54” groups

In short, early retirement is a counter-cultural, powerful way that many thoughtful people bring happiness into their lives. Very few people retire early because it requires pushing back on the cultural norm of spending most of our money on stuff, and instead, saving and investing a much larger percentage of our income than 10-15%. Those pursuing financial independence are buying their freedom out of our consumer culture machine.

Implied assertion 2: The time freedom gained from early retirement prevents us from easily finding purpose and meaning.

I am baffled by this one. The article implies that volunteer activities are somehow not part of early retirement. I disagree. Early retirees can and do an amazing amount of volunteer work in their communities and around the world because they are not tied down to a paid job.

While noble volunteer work is a great idea, it’s not the only way early retirees find meaning. That’s the point: they have time to explore and enjoy a vast array of meaning-making activities. Pursuing hobbies can bring meaning, reward, and joy. When I was working, my full-time job (though meaningful) was choking out what I valued most. I wanted to travel extensively, spend more quality time with my family and friends, read more, learn a language, take better care of my health, and add some whitespace in between these activities.

But my calendar showed a startling gap between what mattered most to me and how I actually spent my time. Our calendars don’t lie. They show us what we actually prioritize, not what we wish we prioritized. I quit my dream job (which was loaded with purpose and meaning) to pursue these higher priorities. I couldn’t be happier because I am following my values and my calendar now reflects these higher values. We don’t need to learn better time management to cut out the things we value to like quality family time so we can keep working; instead we need to challenge our culture that prioritizes work. Early retirement provides a way off of the work-earn-spend treadmill.

Slow traveling to faraway places (which the article dismisses in item 3) and immersing ourselves in different cultures can broaden our perspectives, build goodwill, and help break down fears of immigrants and others who might look or speak differently than we do. I have learned so much as I travel. Meaning and purpose are everywhere, and having time freedom from early retirement has helped me find it.

As early retirees we have more time to volunteer. Here we are at Brother Mouse in Luang Prabang helping Laotian youths learn English—a key to increasing their financial opportunities.

Implied assertion 3: If you haven’t found meaning or purpose in your current work, you shouldn’t retire early, but instead find or create more meaningful work.

Easy to say, but harder to do. Most jobs already have some meaning. Restaurant workers are feeding people and providing a nice dining experience. Housekeepers ensure clean and sanitary places for people to sleep. Car mechanics are helping people get back on the road so they can get to work. Doctors are healing the sick. Lawyers are helping people understand their legal options. But that doesn’t mean those workers want to do that for 40+ years or that this level of meaning is providing the happiness they seek.

Financially successful poets are rare. Thousands (millions?) of blogs, podcasts, and vlogs don’t even cover their basic costs. Most authors don’t get paid for their writing, or not enough to make a living. Most athletes remain amateur. Most small businesses fail. Most people like me with history degrees (and many other degrees for that matter) don’t work in their chosen field but instead work doing something else that pays the bills. Dream jobs are elusive and often don’t present themselves until later in life or without having achieved some form of financial independence to make the leap.

Purpose and meaning are not the sole purview of the working world. I had a very rewarding job educating military service members on personal finance, but I was happy to let go of the staff meetings, office politics, time cards, bureaucratic processes, and hours and hours of annual mandatory training. As an early retiree I still help educate people on personal finance for free and as often as I want, without all of the baggage of working or running my own business. I don’t spend a second thinking about affiliate links, advertising, or selling any of my writing or training, because I don’t want to, and I don’t have to because I pursued financial independence and retired early.

Implied assertion 4: Early retirement rarely makes a person happy.

I am an early retiree. I retired 5 years ago at the age of 52 as did my wife, and we are very happy. I have attended several conferences and meetups within the early retirement community and I have met hundreds of early retirees. Of course troubles come into every life, but on the whole this is the happiest group of people I have ever known, and these people have found strong purpose and meaning in their lives. We have found contentment because we have decided how much money is enough in our lives. We stopped continually adding to the coffers and instead have bought time freedom and full flexibility to pursue what activities we value most.

Working does not make people happier than early retirement. Working for pay at something you find meaningful does not make you happier than doing something you find meaningful (for pay or not) in early retirement. To the contrary, the time freedom of early retirement opens far more possibilities than working does for pursuing the things that make you happy.

Early retirement provides time to have meaningful cross-cultural exchanges with people from around the world. My life is enriched because I travel slowly and learn as I go. Happiness is a nice byproduct.

Early retirement should not be characterized as devoid of purpose and meaning or lumped in as part of mainstream consumer culture. Quite the opposite—reaching full financial independence with the ability to retire early can mean decades of extra time to dedicate to what you value most in life. Sure, a small percentage of people will find (or create) a job that provides more meaning than anything else they could do with their time, and they will continue to do it even if they are financially independent. But for the rest of us who desire a counter-cultural approach, early retirement offers a path to meaning, purpose, and happiness.

[Post Cover Photo Caption: Early retirement has enabled me to have more quality time with family]

I once spent several hundred dollars on a high quality bike rack. It held four bikes, and there were four of us. It seemed like a great investment to increase our family biking time. But pretty quickly I found it was too unwieldy to use. I only used it twice and hated it both times. But instead of letting it go, I stored it and tripped over it in the basement for years even though I knew I would never use it again. I didn’t want to accept the sunk costs of this unfortunate purchase.

The sunk cost fallacy is our tendency to hold onto a purchase or continue with an endeavor we’ve invested money, effort, or time into—even if the current costs outweigh the benefits. I previously wrote about this business concept, but I wanted to expand on how this fallacy impacts what we personally own and why it can be difficult to let things go or do different things with our time. We should not allow the time or money we have previously invested to overly influence our future decisions about time and money.

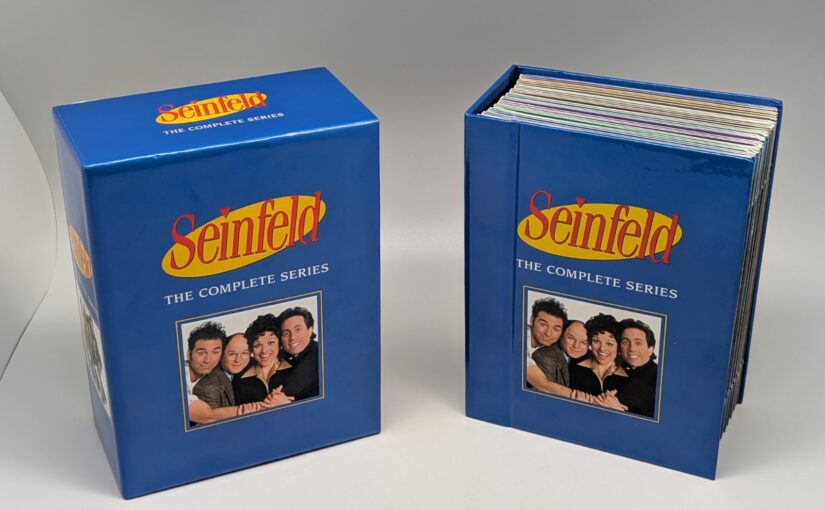

We keep many things because we “paid good money” for them. I purchased the Seinfeld Series DVD box set for something like $120 when it first came out. Even though I made a digital copy of the show, I held onto the set because I believed I should get more than the garage sale price for it. But to recoup more I would need to take a nice photo, research what this item sold for recently ($25-$40), upload it onto a sales website, write a description, handle any inquiries, and then package it up and mail it to the purchaser. I might have made an additional $15-$30 (minus shipping) by doing all that, but I would never recover my $120 and I would end up sinking a lot of my time trying to get that money back. Instead, I accepted the sunk cost and put it in the garage sale—happy for someone to take it away for a few dollars.

Our possessions are most likely not worth near what we had paid for them in the store, and certainly not worth the extra resources required to recover the money sunk into them. I kept many things even though they were not a good fit, because honestly, I didn’t want to admit to my mistake and realize the loss by letting them go.

I have fallen into this fallacy on so many purchases. I can’t tell you all of the new or barely used items (clothes, cans of paints, collectibles, decor items, solvents, hardware, tools, kitchenware, and various other stuff) I kept only because I had sunk money into them and thought “someday” I could recover my investment. Once I accepted that they were expenses, not investments, and the money sunk into them was not coming back, it was easier to let them go.

The sunk cost fallacy often applies to non-refundable purchases. If we have non-refundable tickets to a show and then we miss the show at the last minute, the cost of that ticket is a sunk cost. But this sunk cost should not impact our decision whether we buy another ticket to the same show. I have to remind myself that purchases I made in the past should not prevent me from doing something different now or in the future, even if I can’t get my money back.

Sunk cost fallacy can apply to time, too.

The sunk cost fallacy can apply to things that we have sunk a lot of time into. Letting the sunk cost fallacy determine what we keep can negatively impact what we do with our time and add mental clutter. The weight of spending well over $1,000 on my electric guitar, amp, and hours of lessons was keeping me from moving on to higher priorities even though I knew I no longer prioritized learning to play the guitar.

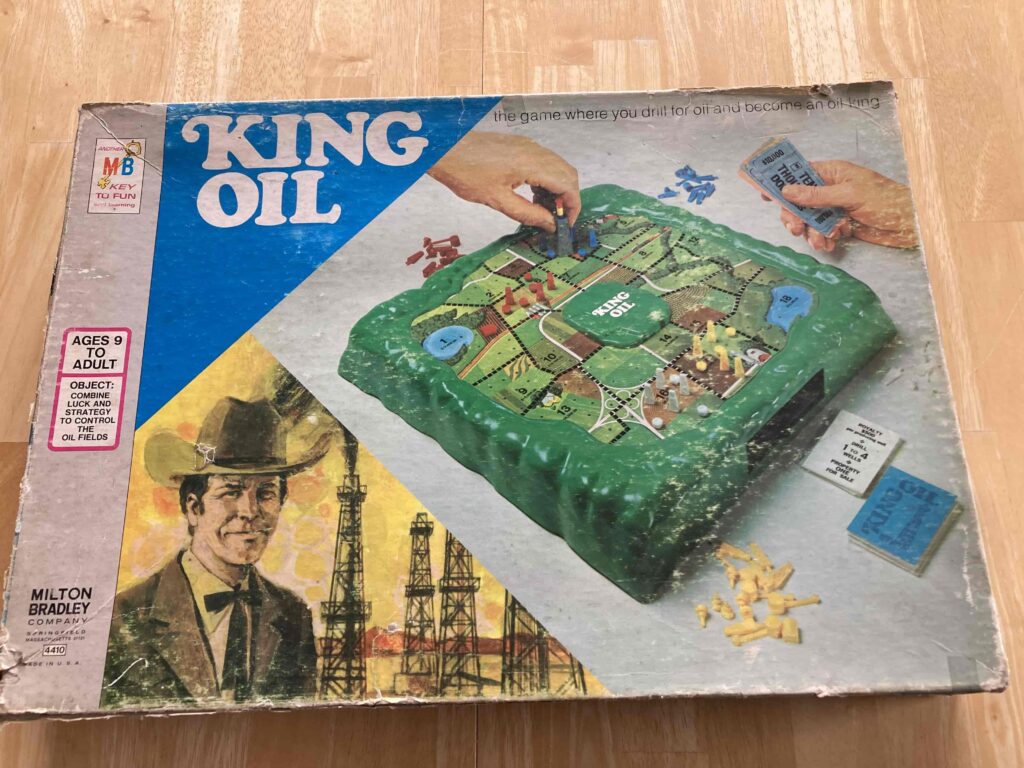

I projected extra value on items that I spent a lot of time on. Items that I had frequently cleaned, maintained, organized, and stored assumed an extra weight of importance since I sunk my time into them. Our old board games that I loved playing like King Oil and Careers were not any more valuable because I had spent hours playing them in my childhood. The same goes for my old kitchenware, musical instruments, college papers, CDs and DVDs. This applies to projects as well. If it is time to sell our house, I shouldn’t let my time spent on numerous home projects and memories of raising our family there keep us in a house that no longer meets our needs today or in the future.

One of my favorite games as a kid — I thought it was worth “good” money as a “classic” game

Look out for sunk cost fallacy’s cousin, the endowment effect.

A related issue is the Endowment Effect, when we value things more just because we own them. We endow our physical possessions with extra value and meaning that we wouldn’t apply to the same items that we didn’t own. We keep many items just because they are ours. I had a lot of clothes like this.

To help me overcome this effect, I had to ask myself if I would pay money to buy that same item again. If this exact shirt was for sale at a store, would I buy it? When I realized that I wouldn’t, it made it easier to donate them. Just because we own it, doesn’t make something more valuable.

Avoid doubling down on bad decisions.

The sunk cost fallacy took control of my decisions when I made one of my worst investing mistakes—purchasing Boston Chicken stock.

In 1997, I purchased 1,000 shares of Boston Chicken (later known as Boston Market). Unfortunately, the company was cooking more than delicious chicken. Just weeks before I purchased the stock (and unbeknownst to me), the company revealed it was recycling money by loaning to its franchisees to build new restaurants, masking its true, troubling financial picture—huge debt.

Boston Chicken soon filed for bankruptcy. I quickly understood that I had made a bad investment decision, but I was afraid to sell and lock in my losses. By letting my desire to recoup my initial investment (at this point a sunk cost) drive my decision, I experienced even greater losses. I watched that stock drop from around $5 per share to pennies as the company financially collapsed. By repeatedly not selling week after week as it plummeted, I let my sunk cost from one bad decision drive more bad decisions.

If we make a bad decision, understanding the sunk cost fallacy helps to see it for what it is, own the mistake and get out of it, resisting the urge to double-down because of a fear of losing what we have invested so far. We should cut our losses and redirect our future resources to something better.

Even good decisions can become susceptible to the sunk cost fallacy.

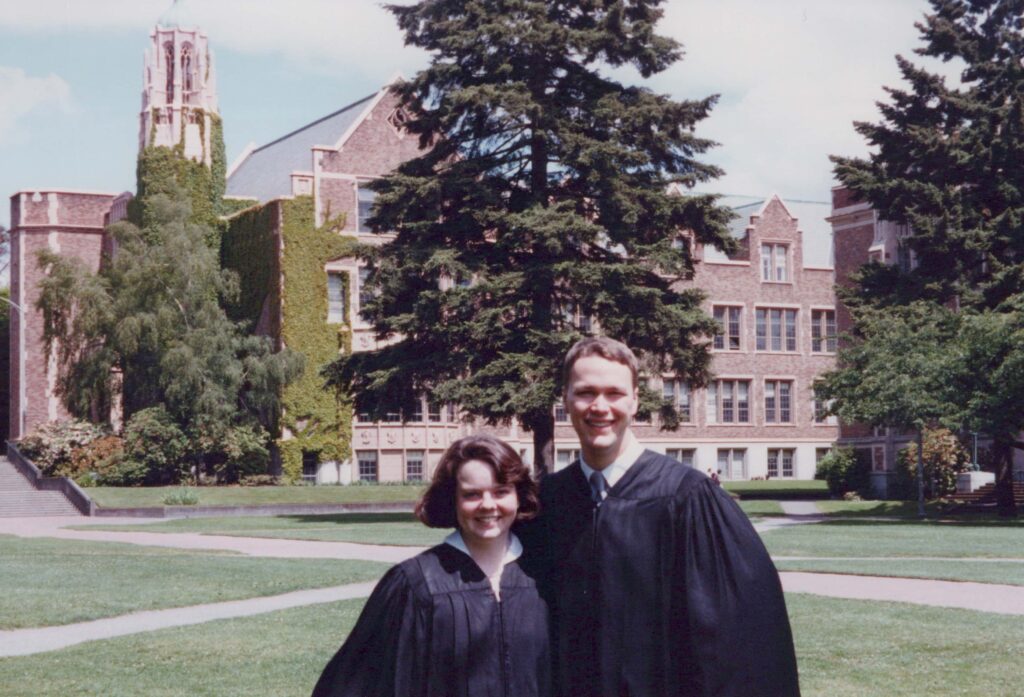

Sometimes decisions are good in the moment, but they can trap us in the sunk cost fallacy later. For example many of us, me included, earned a degree in a field that we didn’t end up working in (mine was history). Spending money and time getting a particular degree is a sunk cost. If the job opportunities that present themselves are in different fields or we decide we want to do something different, we should not let those sunk educational costs prevent us from going in a different direction.

Launa and I on graduation day

I was able to set aside the weight of my sunk costs (time, knowledge, and commitment to the organization) and quit my dream job to instead pursue what I valued more—travel, more quality time with family and friends, my health, and following my curiosities to include learning more about human history.

Decisions in the past, even good ones, that we put a lot of money and time into can sometimes cause us to limit our options. We need to recognize that these are sunk costs and consider other opportunities even if it means setting these previous investments aside.

Is there something you’re currently keeping or spending time on, and you’re doing so because of the time or money you already have invested? If so, consider stepping back and evaluating if sunk cost fallacy is preventing you from decluttering or managing your time. Recognize that the time and money already spent is gone, but we can make a fresh start with how we spend these valuable resources going forward.

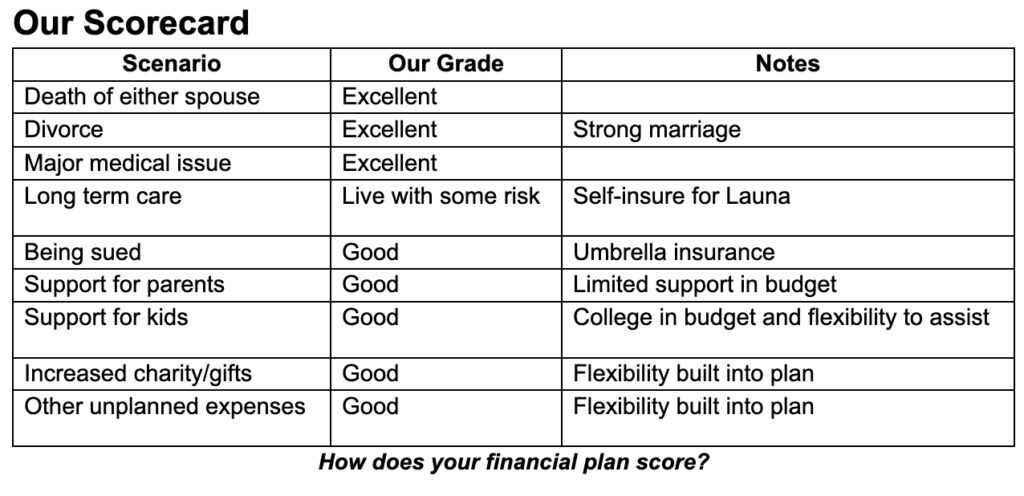

Several prominent early retirees have shared their challenges with life-changing events to include divorces, major medical surprises, and death of a spouse. While these events have a low chance of occurring for most early retirees, the impact of these events could derail our retirement plans. Some early retirees had to return to full-time employment as their passive income no longer covered their expenses. But others had a strong enough financial picture to weather the significant cut in net worth from a divorce, loss of a pension from a spouse’s death, major medical expenses, or unplanned expenses from life changes like getting married and having children. To minimize the impact of unplanned events on our retirement plans, we need to stress test our plans before we retire. While we can’t (and shouldn’t) plan for every possible scenario, having a good idea of our financial options will help us sleep better as we take the leap into early retirement.

Using our current expenses to figure out our financial independence number is a great place to start. As we get closer to achieving financial independence though, we need to refine our projections to account for projected expenses in retirement. The earlier you retire, the harder it will be to get a good handle on these expenses over time. Stress testing for common unplanned events will help.

Before I quit my job and retired early 5 years ago, I first figured out the safe withdrawal rate from our investments and what that would provide in combination with real estate income, pensions, and Social Security (I found this tool by Karsten Jeske at his Early Retirement Now blog to be very helpful in this regard). After that, I ran numerous scenarios to test if my and my wife’s retirement plan would handle major life changes. We needed to know if our retirement would be torpedoed if one of us died unexpectedly early, we got a divorce, had a major health challenge, or other major change in our lives. I had a good estimate of what our projected income would be and knew it would cover our projected known expenses, to include inflation. But I still needed to see how a major unplanned event might impact our plan.

For each of the scenarios below, I conservatively adjusted income and expenses, and assessed how well our adjusted income covered the adjusted expenses. Then I graded how well our financial plan would hold up for each with “Excellent,” “Good,” “Live with some risk,” or “Failing” (i.e., postpone retirement and keep saving). My scenarios are aimed at capturing 80% of worst case scenarios. Trying to cover the rarest and most catastrophic of situations, particularly for medical expenses, would prevent us from ever retiring, and I’m not interested in living with that level of fear.

While every person’s situation is different, hopefully my thought process for stress testing our plan through several scenarios will help you better evaluate your own retirement plan.

Arlington National Cemetery

Early death of either spouse

We wanted to make sure that if one of us passed away that the other person would be financially sound. For joint accounts, if one spouse passes away then the other spouse will generally retain full ownership of the accounts. In our case, if my wife died, all of our assets would remain with me as I am her beneficiary. However, if I died, my military pension and VA disability benefits would disappear as Launa and I smartly turned down the military’s Survivor Benefit Plan. Because of this we made sure we had enough passive income from investments, real estate, and maximum social security to cover her projected expenses (to include higher taxes filing single). We also bought a term life-insurance that would cover our primary house mortgage to hedge against my early death before we had enough invested. If I died tomorrow, she would be financially set because she is individually financially independent. Grade: Excellent.

Divorce